Expect Tax Demand Notice from I-T Dept, ETCFO

On September 19, 2025, the Central Board of Direct Taxes (CBDT) via Circular No. 13 /2025 gave relief to taxpayers from paying interest on tax demand notices related to the Section 87A tax rebate for special rate incomes like Short Term Capital Gains (STCG) on equities. However, the same circular states that taxpayers who received such a tax demand notice must pay by December 31, 2025 so as to become eligible for the waiver of interest.

Additionally, the circular mentions that if the ITR was processed and Section 87A tax rebate was granted on such special rate incomes (like STCG), rectifications have to be done disallowing such 87A tax rebate claims since they were mistakenly approved. Consequently, that circular said that tax demand notices will be issued, and interest under Section 220(2) will be applied to these tax demands.

S. Vasudevan, Executive Partner at Lakshmikumaran & Sridharan attorneys, says: “The CBDT in its recent circular (13 of 2025) has stated that rectifications have to be carried out by Central Processing Center (CPC) to disallow Section 87A tax rebate which was allowed to the taxpayers against income chargeable to tax at special rates. Considering this recent Circular issued by CBDT, it is likely that taxpayers will receive a demand notice with respect to rebate allowed under section 87A.”

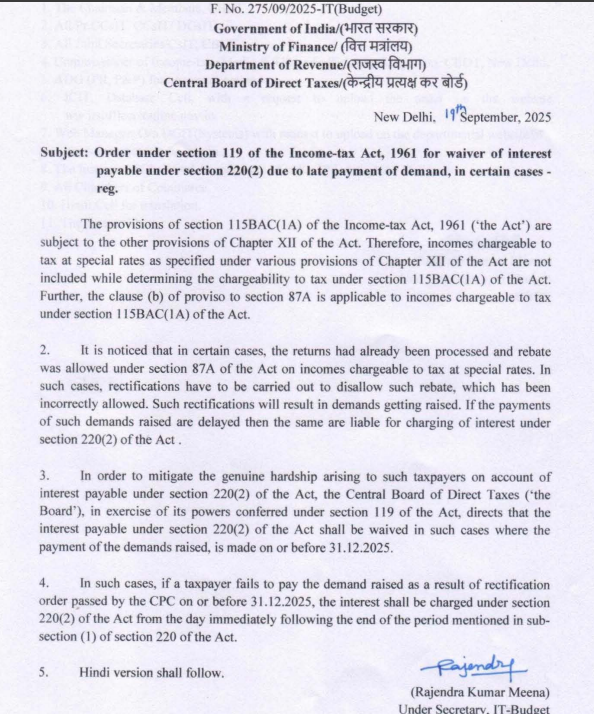

The relevant portion of the circular can be found below:

Source: The circular 13 of 2025.

Also read: Demand for extension of due date of tax audit report and ITR filing is getting wider with many tax bodies writing to finance minister and PMO

What can taxpayers do?

Vasudevan of Lakshmikumaran & Sridharan attorneys says that the circulars of the CBDT bind taxation authorities and not the taxpayers. Vasudevan says that it has been settled law that a circular cannot impose a higher burden than what the Income-tax Act itself, on a true interpretation, envisages.

Also read: No tax for wife who sold house for Rs 2.85 crore and bought another house jointly with husband, rules ITAT Mumbai

Vasudevan says: “The Circular empowers CPC to issue rectification orders and raise tax demand in cases where 87A rebate has been allowed to the taxpayers. However, the taxpayer receiving such notice, can litigate the matter by filing an appeal before Commissioner of Income-tax (Appeals). The taxpayers can continue to defend their case by placing reliance upon the favorable ITAT decisions.”

Also read: Higher EPS pension for EPF members allowed by Punjab & Haryana High Court for pre-2014 retired employees with these three conditions

Neeraj Agarwala, Partner, Nangia & Co LLP, says that the concern raised is valid. Taxpayers who claimed rebate on special-rate income should expect demand notices. The law specifically states that rebate under Section 87A is not available on long-term capital gains under Section 112A (above Rs 1.25 lakh). However, the law does not explicitly exclude short-term capital gains under Section 111A or other special-rate incomes. Many taxpayers therefore claimed rebate against such incomes in good faith.

Agarwala adds: “However, the income tax department has consistently taken the view that Section 87A rebate applies only to tax on slab-rate income, not on income taxed at special rates. With the recent circular, the department has reiterated its stand that rebate under Section 87A is not available against any income taxed at special rates. As a result, taxpayers who claimed the rebate on such income may now receive demand notices. In fact, circular further provides that even if the returns were earlier processed without objection, taxpayers may now see demand notices reversing the benefit. Such demands would need to be discharged by 31 December 2025; while interest for delayed payment will be waived.”

Mihir Tanna, associate director, S.K Patodia LLP says: “This circular provides indication to those taxpayers who could have claimed Section 87A tax rebate on STCG income prior to July 5, 2024. These taxpayers will get a tax notice for claiming Section 87A tax rebate. After the judgment of Bombay High Court for restricting 87A claim in ITR and several lower court judgments allowing 87A, relief was expected from the income tax department. However, by issuing this circular department, it is clear that litigation on 87A is likely to increase. Circular gives marginal relief that even if the tax payer doesn’t pay demand within 30 days of receiving this tax notice, interest at 1% per month will not be payable. This present circular (13/2025) has waived off the interest, if the taxpayer pays the tax demand on or before December 31, 2025.”

Agarwala says: “The circular is significant as it cements the tax administrative stand against allowing Section 87A rebate on income taxed at special rates. It is important to note that while circulars are binding on the tax department, they cannot override the provisions of the Income-tax Act. Accordingly, taxpayers may opt to contest such demands and await the decision of higher courts to settle this dispute.”

Also read: Granddaughter says father and aunt denied her share in grandfather’s property; Delhi Court quotes Hindu Succession Act to reject her claim

What did the recent ITAT Ahmedabad ruling about Section 87A say?

According to the Income Tax Appellate Tribunal (ITAT) Ahmedabad order dated August 12, 2025, here’s what they said:

- “…we find that the assessee is a resident individual and the total income declared for the assessment year 2024–25 does not exceed Rs.7,00,000. It is also an admitted position that the assessee has exercised the option to be assessed under the new tax regime in accordance with the provisions of section 115BAC(1A).

- “On a plain reading of the statutory provisions, there exists no express bar either in Section 87A or Section 111A for denial of rebate in respect of tax payable on short-term capital gains arising from transfer of listed equity shares taxable at special rates under Section 111A.”

- “The legislative intent is further clarified by the subsequent amendment proposed in the Finance Bill, 2025, which is prospective in nature and thereby reinforces that no such restriction was in force during the relevant assessment year.”

- “The denial of rebate under Section 87A by the CPC, Bengaluru, appears to be based solely on system-driven logic and not on any statutory mandate. Moreover, the interpretation adopted by the CIT(A) in upholding such denial is, in our considered view, not in consonance with the plain and unambiguous language of the law as applicable for A.Y. 2024–25.”

What is the issue that is causing such problems regarding claiming of 87A tax rebate

According to an earlier Economic Times report dated July 21, 2024, the ITR filing utilities stopped allowing tax rebate under Section 87A for various special rate incomes including short-term capital gains on equity shares or equity-oriented mutual funds taxable at 15% under Section 111A.

“Earlier the Income Tax Utility Software allowed filing of ITRs with rebate, but after July 5, 2024, a whole controversy arose due to change of schema of utility software by the income tax department. Pursuant to those ITRs which were filed with tax rebate are now getting intimation notices for tax demand equivalent to amount to rebate availed. Recently, more than 500 demand notices were received by members of Chartered Accountants Association Surat. Where there was a refund due, the amount of rebate was deducted from it after processing of the ITR,” said CA Hardik Kakadiya, President, Chartered Accountants Association Surat in an earlier story.